Many of us underestimate the need for insurance. Sometimes it’s also due to sheer ignorance of what is available to us.

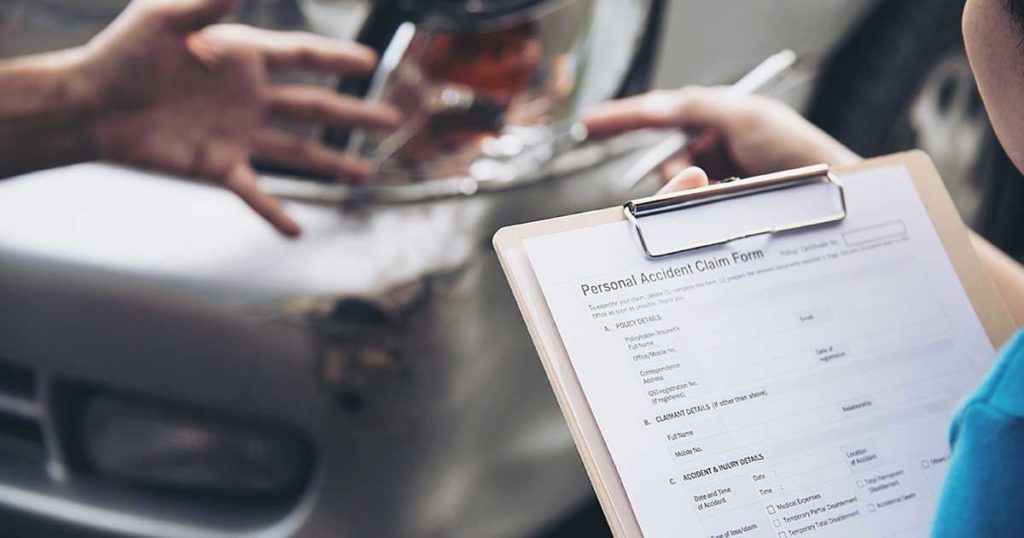

I never had the right head for finances. So it was no small wonder that I treated insurance agents with a deep-rooted sense of mistrust. But then my friend met with an accident. I was worried. Where would she get the money for the hospital expenses? How much could I help, if at all? But my friend waved my concerns aside. “I have insurance,” she said from her hospital bed. “But thanks for the concern.”

That set me thinking and I plunged into the world of finance and insurance. Sure enough, I found everything as daunting as ever, but things slowly started to make a little more sense. And even though I can’t ever claim to be an expert, I have understood that everyone needs to plan their finances and take some kind of insurance.

So here are some basic things to set you on your own path of discovery.

The insurance jargon:

- Premium: The money you pay to the insurance company. It may be a one-time payment, an annual, quarterly, or even monthly payment.

- Insured and insurer: the person who takes the insurance policy or the one in whose name the policy is made is the “insured”. The company selling you insurance is the “insurer”. In addition to this, there is usually a “nominee” or the person who gets the benefits in the event of the death of the “insured”.

- Sum assured: this is the guaranteed amount of money the insurance company will pay to you. It doesn’t include the bonuses.

- Maturity value: The money you get when the policy completes its term.

- Bonus: The additional amount of money that is given to you at various intervals. It varies from company to company.

- Rider: An optional feature of the insurance policy that you may/may not opt for. You will have to pay a little extra for the rider. For example, a life insurance policy may come with an accident insurance rider.

- Annuity: This refers to a guaranteed fixed payment that the insurance company makes to you at some future date.

- Surrender value: What you will get if you decide to discontinue the policy midway.

Insurance companies will garb these basic terms into smart and often complicated terms. But if you understand these you can find your way around a bit more comfortably.

Apart from life insurance, depending on your priorities you can choose from:

- Health Care Insurance: With the spiraling medical costs this is the most important of insurance policies.

- Auto Insurance: This insurance is for accident or theft of your car or any other vehicle that you drive.

- Travel Insurance: This becomes more important when you travel internationally or go for adventure treks.

- Business Insurance: There is a gamut of insurance policies to take care of the needs of various businesses from property insurance to liability insurance.

- House Insurance: Insurance against theft, accidents, and natural disasters that may strike your home.

Remember also that insurance premiums will vary depending on your age, health, and job profile. So first do your basic research, list out your priorities, and then only approach an insurance agent. When in doubt, ask.

Information on sites such as Economy Watch helped me put together a clear picture of insurance here. There are many other useful sites that can help guide you in your quest for the right product.