With the instability of government programs and rising seniors now caring for their aging parents, many people are beginning to think seriously about their Long Term Care (LTC) Insurance options. People want to have some peace of mind that their needs will be met when they are unable to care for themselves. If you are considering LTC insurance, here’s what you need to know and how you should go about choosing the right policy for your needs:

What is Long Term Care Insurance?

Long Term Care Insurance is an insurance product that helps pay for costs associated with medical care and services that are generally not covered by health insurance or Medicare. With LTC, these services can be rendered in an assisted living facility, private home, or nursing home as well as in an acute hospital setting.

Is Long Term Care (LTC) relevant?

Long Term Care Insurance is a relatively new concept. In fact, it has only been offered by insurance companies since the 1980s when insurance professionals saw that lengthened life expectancies resulted in an increased need for intermediate and custodial care, which was not covered by traditional health insurance policies. Generally, Long Term Care Insurance is meant to bridge the gap between traditional health insurance and uninsured (or under-insured) medical expenses.

How to shop for an insurance agent

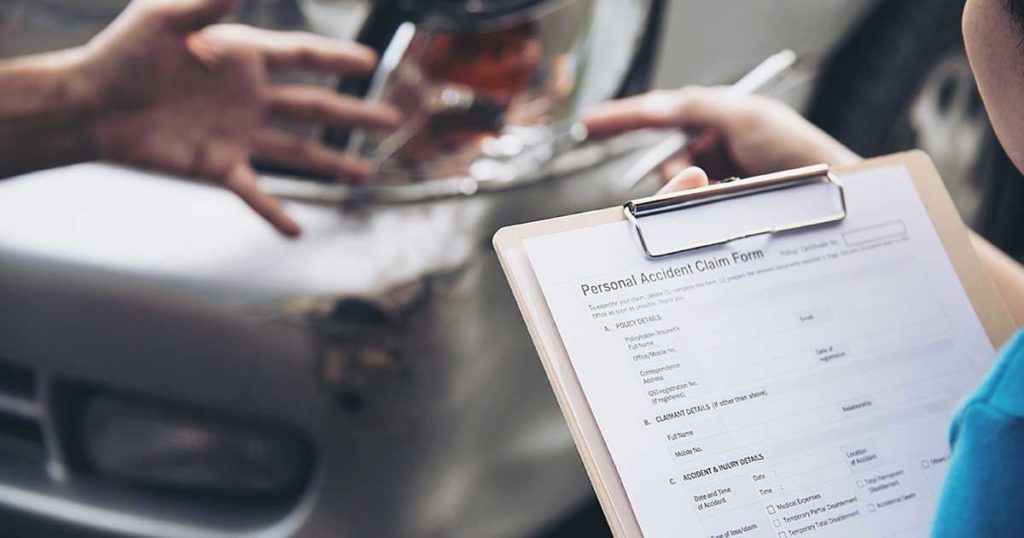

It goes without question that choosing the best product for your needs goes hand-in-hand with choosing the right insurance agent; therefore, it is best not to make this decision in haste. The insurance industry is flooded with capable sales professionals offering different products and services to help you with your goals.

Look for a reputable agent and company. You can do this by asking for personal referrals from family, friends, and coworkers. You can also find the Financial Stability Ratings (FSRs) for each insurance company on your list on your state’s insurance department website. These ratings will help you understand the financial solvency of each company. Low FSRs are a sign of financial trouble and a red flag that you should take your business elsewhere.

You should also take some time to consider if you’d like to work with an insurance agent that sells a specific line of products within one corporate brand (Captive Agent) or an independent insurance agent (Noncaptive Agent) that sells a variety of products from several different companies. This is a matter of preference and you should include agents from both sides if you’d like to get an idea of which option will work best for you.

Review your agent’s recommendations

Things to look for:

- The policy should allow skilled and unskilled labor—health aides, for example.

- The policy should cover you for at least one year.

- Make sure you won’t have to be hospitalized before you can receive benefits.

- Ensure the policy won’t be canceled or become unrenewable as you age or become ill.

- Make sure the policy offers inflation protection.

Research and ask questions

Your policy is a legally binding contract between you and your insurance provider. If you have questions, you should ask and look for evidence in the written policy. Make sure you understand the contents of the policy before signing it. It is perfectly reasonable to take additional time (perhaps overnight) to review the documents thoroughly before signing them.

Review your policy regularly

While choosing a Long Term Care Insurance policy will take some time and legwork on your part, your approach should be consistent. You will need to evaluate your policy against your needs each time your policy renews. If either the policy or your needs have changed, start this evaluation process all over again.